Synonyms

More meanings

Tip: select a single word for meaning & synonyms.

Select multiple words normally to copy text.

Here, you will find summaries, questions, answers, textbook solutions, pdf, extras etc. of (Nagaland Board) NBSE Class 12 (Arts/Commerce) Economics Chapter 1: Introduction. These solutions, however, should be only treated as references and can be modified/changed.

Economics is a fascinating field of study that is divided into two major branches: Microeconomics and Macroeconomics. Microeconomics focuses on the behavior of individual economic units, such as households, firms, or industries. It delves into how these units make decisions, considering factors like scarcity and resource allocation. On the other hand, Macroeconomics takes a broader view, studying the economy as a whole. It examines aggregates and averages of the entire economy, such as national income, total employment, aggregate savings and investment, aggregate demand, aggregate supply, and the general price level.

The field of macroeconomics was revolutionized by the British economist J.M. Keynes, who authored the book “General Theory of Employment, Interest and Money” in 1936. This work, which came in response to the Great Depression, challenged the classical assumption of full employment and led to the development of Macroeconomic Theory. Keynes’ ideas have had a profound impact on economic thought and policy-making, underscoring the importance of macroeconomics in understanding and managing economies.

Macroeconomics is crucial for several reasons. It helps us understand the functioning of a complex modern economy, the interdependence of various sectors, the causes of short-run fluctuations in output and employment, and the causes of long-run economic growth. It also aids in formulating economic policies to promote economic growth, reduce unemployment and inflation, and promote a stable and well-functioning economy.

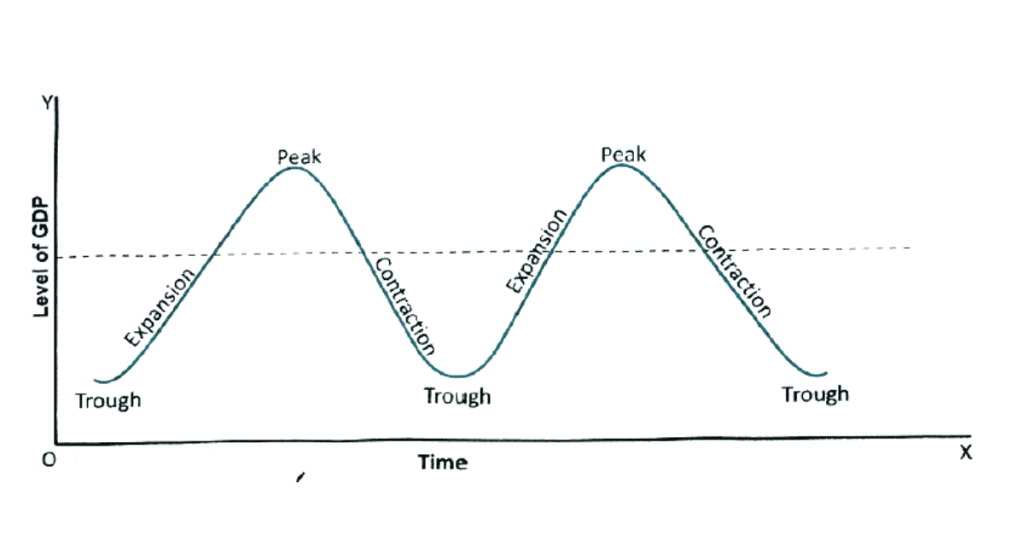

One of the key concepts in macroeconomics is the business cycle, which refers to the short-run fluctuations in economic activity. The business cycle consists of four phases: expansion (or recovery), peak, contraction (or recession), and trough. Understanding the business cycle is crucial for policy-making and for businesses and investors.

Another important concept in economics is the distinction between final goods and intermediate goods. Final goods are those that are meant for final use by consumers or for investment by firms. They are not used for further transformation or resold. Intermediate goods, on the other hand, are used as raw material for further production of other goods or for resale in the same year. This distinction is important because the national income includes the value of only final goods, not intermediate goods.

Economics also differentiates between flow variables and stock variables. Flow variables are measured per unit of time, such as income or output per year. Stock variables, on the other hand, are measured at a particular point in time, like wealth or debt.

1. Name the two branches of economics.

Answer: The two branches of economics are Microeconomics and Macroeconomics.

2 Name the book authored by J.M. Keynes to explain macroeconomic theory.

Answer: The book authored by J.M. Keynes to explain macroeconomic theory is “General Theory of Employment, Interest and Money”.

3. State the meaning of microeconomics

Answer: Microeconomics is that part of economic theory which studies the behaviour of individual economic units of an economy such as a household, a firm, an industry, etc.

4. State the meaning of macroeconomics.

Answer: Macroeconomics is the study of national aggregates or economy-wide aggregates. It revolves around determination of the level of income and employment, therefore, it is also known as ‘Theory of Income and Employment’.

5. “Study of inflation” is a macroeconomic concept. True or false.

Answer: True

6. Define Aggregate Demand.

Answer: Aggregate Demand is the demand for final goods and services in an economy at a given time.

7. What do you mean by Aggregate Supply?

Answer: Aggregate supply is the total supply of goods or services that firms in a national economy plan on selling during a specific time period.

8. “Purchase of a refrigerator by a firm”. Here, refrigerator is a capital good or a consumption good?

Answer: The refrigerator is a capital good.

9. “Bread is a consumer goods”. True or false.

Answer: True.

1. Define Economics.

Answer: Economics is the study of how societies use scarce resources to produce valuable goods and services and distribute them among different people. It primarily focuses on the interaction between economic agents and how economies work.

2. What do you mean by Microeconomics?

Answer: Microeconomics is that part of economic theory that studies the behaviour of individual economic units of an economy such as a household, a firm, an industry, etc. It is the analysis of the economy’s constituent elements-households, firms, and industries.

3. What do you mean by Macroeconomics?

Answer: It is that part of economic theory that studies the economy in its totality or as a whole. It studies not individual economic units like a household, a firm or an industry but the whole economic system. Macroeconomics is the study of aggregates and averages of the entire economy.

4. Divide each of the following into macroeconomics or microeconomics concepts:

(i) Employment level in the country

Answer: Macroeconomics

(ii) Inflation rate in an economy

Answer: Macroeconomics

(iii) Salary of an individual

Answer: Microeconomics

(iv) Price of tomato in Delhi

Answer: Microeconomics

5. What is meant by business cycle?

Answer: The business cycle is also known as the economic cycle or trade cycle, it is the downward or upward movement of gross domestic product around its long-term growth trend.

6. How are producer goods different from capital goods?

Answer: All goods which are used in the production of other goods are termed producer goods. On the other hand, capital goods include only fixed assets of producers which are usually of high value. Thus, all capital goods are producer goods but all producer goods are not capital goods.

1. What is the importance of macroeconomics?

Answer: Macroeconomics enriches our knowledge of the functioning of an economy by studying the behavior of national income, output, investment, savings, and consumption. It helps in solving the problems of inflation, unemployment, economic instability, and economic growth.

2. Explain the concept of the business cycle with the help of a diagram.

Answer: The business cycle, also known as the economic cycle or trade cycle, is the downward or upward movement of gross domestic product around its long-term growth trend.

3. Differentiate between aggregate demand and aggregate supply.

Answer: Aggregate Demand is the demand for final goods and services in an economy at a given time. It specifies the amounts of goods and services that will be purchased at all possible price levels. This is the demand for the gross domestic product of an economy. On the other hand, Aggregate supply is the total supply of goods or services that firms in a national economy plan on selling during a specific time period. It is the total amount of goods and services that firms are willing and able to sell at a given price level in an economy.

4. Explain the concept of final goods and intermediate goods by giving examples.

Answer: All goods which are meant either (a) for consumption by consumers or (b) for investment by firms are called final goods. Eg., A car purchased for personal use.

All goods which are used (a) as raw material for further production of other goods or (b) for resale in the same year are known as intermediate goods. Eg., A machine bought for resale.

5. Discuss the four sectors of an economy.

Answer: The four sectors of an economy are:

(a) Household Sector: It consists of consumer goods and services and households are also owners of the factors of production.

(b) Producer Sector: It consists of firms, i.e. all producing units in the economy. Firms hire factors of production, i.e. Land, Labour, Capital and Entrepreneurial skills from the households for the production of goods and services.

(c) Government Sector: The government performs various welfare functions as maintaining law and order and defence.

(d) Rest of the world: It is also called the external sector. It includes all such activities which are related to the export and import of goods and capital between the domestic economy and the rest of the world.

6. Write a short note on the basic problems of an economy.

Answer: The basic problems of an economy are economic growth, inflation, and unemployment. Economic growth refers to the increase in the economy’s production over a period of time. Inflation refers to a situation of constantly rising prices of commodities and factors of production in the economy. Unemployment refers to the situation where the labour is able as well as willing to work but is sitting idle due to the unavailability of any work opportunity.

1. Differentiate between microeconomics and macroeconomics.

Answer: Microeconomics is that part of economic theory that studies the behaviour of individual economic units of an economy such as a household, a firm, an industry, etc. It is the analysis of the economy’s constituent elements-households, firms, and industries. On the other hand, macronomics is that part of economic theory that studies the economy in its totality or as a whole. It studies not individual economic units like a household, a firm or an industry but the whole economic system. Macroeconomics is the study of aggregates and averages of the entire economy.

2. Explain how consumption goods are different from capital goods.

Answer: Consumption goods are goods which are consumed for their own sake or which satisfy current wants of consumers directly. Examples include food, shirts, shoes, cigarettes, pens, TV-sets, radio, services of a doctor, etc. They are further classified into durable and non-durable goods. Capital goods, on the other hand, are fixed assets of producers which are repeatedly used in the process of production for several years. They are used for generating income by production units. Examples include tools, implements, machinery, plants, tractors, buildings, transformers, etc. They undergo wear and tear and need repairs or replacement over time.

3. Differentiate between flow variables and stock variables.

Answer: Flow variables are quantities that are measured with reference to a period of time. They have a time dimension. For instance, national income is a flow as it describes and measures the flow of goods and services which become available to a country during a year. Other examples of flows include expenditure, savings, depreciation, interest, exports, imports, change in inventories, change in money supply, rent, profit, etc.

On the other hand, stock variables are quantities that are measurable at a particular point of time. For instance, capital is a stock variable. On a particular date, a country owns and commands a stock of machines, buildings, accessories, raw materials, etc. It is the stock of capital. A stock has a reference to a particular date on which it shows the stock position. A stock has no time dimension. Examples of stocks are wealth, foreign debts, loan, inventories, opening stock, money supply, population, etc.

1. Define macroeconomics. What is the importance of macroeconomics?

Answer: Macroeconomics is that part of economic theory that studies the economy in its totality or as a whole. It studies not individual economic units like a household, a firm or an industry but the whole economic system.

The importance of macroeconomics are:

i. It helps to understand the functioning of a complicated modern economic system.

ii. It helps to achieve the goal of economic growth, a higher level of GDP and a higher level of employment.

iii. It helps to bring stability to the price level and analyses fluctuations in business activities. It suggests policy measures to control inflation and deflation.

iv. It explains factors which determine the balance of payment. At the same time, it identifies causes of deficit in the balance of payment and suggests remedial measures.

v. It helps to solve economic problems like poverty, unemployment, business cycles, etc., whose solution is possible at the macro level only, i.e. at the level of the whole economy.

vi. With detailed knowledge of the functioning of an economy at the macro level, it has been possible to formulate correct economic policies and also coordinate international economic policies.

vii. Last but not least, macroeconomic theory has saved us from the dangers of the application of microeconomic theory to the problems of the economy as a whole.

2. Write a note on Business Cycle.

Answer: The business cycle, also known as the economic cycle or trade cycle, is the downward or upward movement of gross domestic product around its long-term growth trend. In other words, it describes the rise and fall in the production of goods and services in an economy. The period of high income, output, and employment is called the period of expansion or prosperity, and the period of low income, output, and employment is described as a period of contraction or depression.

These alternating periods of expansion and contraction in economic activity have caused the business cycle. The duration of a business cycle has not been of the same length; it has varied from a minimum of two years to a maximum of twelve years.

There are four phases of the business cycle:

(i) Expansion (Boom or prosperity)

(ii) Peak (upper turning point)

(iii) Contraction (Downsizing, Recession)

(iv) Trough (or Depression) (lower turning point).

After remaining at the trough for some time, the economy revives and again the new cycle begins.

3. How consumption goods are differentiated from capital goods?

Answer: All final goods produced in the economy are of two kinds – consumption goods and capital (investment) goods. Consumption goods are goods which are consumed for their own sake or which satisfy current wants of consumers directly. For example, food, shirts, shoes, cigarettes, pens, TV-sets, radio, services of a doctor, etc. are all consumer goods because when used, they satisfy immediate needs of consumers. These include both purchased goods and goods produced on their own.

On the other hand, capital goods are fixed assets of producers which are repeatedly used in the production process for several years. Such goods are used for generating income by production units. These goods are of durable character, e.g., tools, implements, machinery, plants, tractors, buildings, transformers, etc. They make production of other goods possible, they themselves do not get transformed (or merged) in the production process, they undergo wear and tear (i.e., depreciate) and need repairs or replacement over time, and they are the backbone of production processes as they aid and enable production to go on continuously.

4. Differentiate between the followings:

(a) final goods and Intermediate goods.

Answer: Final goods are all goods which are meant either for consumption by consumers or for investment by firms. They are meant for final use and the final users of a product are consumers and producers. They are neither used for further transformation in production nor resold. In other words, final goods are acquired for their own use, i.e. by consumers for satisfaction of their wants and by producers for capital formation.

On the other hand, intermediate goods are all goods which are used as raw material for further production of other goods or for resale in the same year. Intermediate goods are purchased by one firm from the other for use as raw material or for resale. The basis of distinction between final and intermediate goods is the end use made of the good, not the good itself. Goods purchased and used up in production process or resold during the same year are intermediate goods whereas goods purchased for consumption or for investment are called final goods.

(b) flow and stocks.

Answer: Flow variables are quantities which are measured with reference to a period of time. Flows are defined with reference to a specific period (length of time), e.g., hours, days, weeks, months or years. It has time dimension. National income is a flow. It describes and measures flow of goods and services which become available to a country during a year. All other economic variables which have time dimension, i.e. whose magnitude can be measured over a period of time are called flow variables.

On the other hand, stock variables are quantities which are measurable at a particular point of time. Capital is a stock variable. On a particular date, a country owns and commands stock of machines, buildings, accessories, raw materials, etc. It is stock of capital. Like a balance sheet, a stock has a reference to a particular date on which it shows stock position. Clearly, a stock has no time dimension (length of time) as against a flow which has time dimension. A flow shows change during a period of time whereas a stock indicates the quantity of a variable at a point of time. Thus, wealth is a stock since it can be measured at a point of time, but income is a flow because it can be measured over a period of time.

5. What is the importance of macroeconomics?

Answer: The importance of macroeconomics is manifold:

i. It helps to understand the functioning of a complicated modern economic system. It describes how the economy as a whole functions and how the level of national income and employment is determined on the basis of aggregate demand and aggregate supply.

ii. It helps to achieve the goal of economic growth, higher level of GDP and higher level of employment. It analyses the forces which determine economic growth of a country and explains how to reach the highest state of economic growth and sustain it.

iii. It helps to bring stability in price level and analyses fluctuations in business activities. It suggests policy measures to control inflation and deflation.

iv. It explains factors which determine balance of payment. At the same time, it identifies causes of deficit in balance of payment and suggests remedial measures.

v. It helps to solve economic problems like poverty, unemployment, business cycles, etc., whose solution is possible at macro level only, i.e. at the level of the whole economy.

vi. With detailed knowledge of functioning of an economy at macro level, it has been possible to formulate correct economic policies and also coordinate international economic policies.

1. What are the two major branches of economics?

Answer: There are two major branches of economics, namely, Microeconomics and Macroeconomics.

2. What is microeconomics?

Answer: Microeconomics is the study of the behaviour of individual economic units of the economy. It is that part of economic theory which studies the behaviour of individual economic units of an economy such as a household, a firm, an industry, etc. It is the analysis of the economy’s constituent elements—households, firms, and industries.

3. What is macroeconomics?

Answer: Macroeconomics is the study of the behaviour of the economy as a whole and its aggregates. It is that part of economic theory which studies the economy in its totality or as a whole. It studies not individual economic units like a household, a firm or an industry but the whole economic system. Macroeconomics is the study of aggregates and averages of the entire economy.

4. What are the two main schools of economic thought?

Answer: There are two main schools of economic thought—Classical School and Keynesian School.

5. What is the Keynesian School of thought?

Answer: The Keynesian School of thought originated from the work of the British economist J.M. Keynes. He criticised the Classical assumption of full employment and developed a new theory known as Macroeconomic Theory, which brought about a revolution in economic thought called the Keynesian Revolution.

6. What event defied the classical doctrine of automatic full employment?

Answer: The Great Depression of the early 1930s (1929–33) defied the myth that the automatic working of the market mechanism would ensure an equilibrium level of income consistent with full employment of resources.

7. Who was J.M. Keynes?

Answer: J.M. Keynes was a well-known British economist.

8. What is the name of the famous book written by J.M. Keynes?

Answer: The name of the famous book written by J.M. Keynes is “General Theory of Employment, Interest and Money”.

9. When was the “General Theory of Employment, Interest and Money” published?

Answer: The “General Theory of Employment, Interest and Money” was published in 1936.

10. What is the Keynesian Revolution?

Answer: The Keynesian Revolution refers to the revolution in economic thought brought about by J.M. Keynes’s famous book “General Theory of Employment, Interest and Money”, published in 1936.

11. What are the main tools of analysis in macroeconomics?

Answer: The main tools of analysis in macroeconomics are aggregate demand and aggregate supply of the economy as a whole.

12. What are some examples of economic aggregates?

Answer: Examples of economic aggregates are national income, total employment, aggregate savings and investment, aggregate demand, aggregate supply, and the general price level.

13. How does macroeconomics help in achieving economic growth?

Answer: Macroeconomics helps to achieve the goal of economic growth, a higher level of GDP, and a higher level of employment. It analyses the forces which determine the economic growth of a country and explains how to reach the highest state of economic growth and sustain it.

14. How does macroeconomics help in maintaining price stability?

Answer: Macroeconomics helps to bring stability in price level and analyses fluctuations in business activities. It suggests policy measures to control inflation and deflation.

15. What is the subject matter of microeconomics?

Answer: The subject-matter of microeconomics deals with:

(i) determination of prices of individual products and factors; and

(ii) allocation of resources to their most valuable uses so as to maximise the total output of the economy.

16. What is the central problem of microeconomics?

Answer: The central problem of microeconomics is price determination and allocation of resources.

17. What is the central problem of macroeconomics?

Answer: The central problem of macroeconomics is the determination of the level of national income and employment.

18. What are the main tools of microeconomics?

Answer: The main tools of microeconomics are the demand and supply of a particular commodity/factor.

19. What are the basic problems of an economy at the macroeconomic level?

Answer: The basic problems of an economy at the macroeconomic level are Economic Growth, Inflation and Unemployment.

20. What is economic growth?

Answer: Economic Growth refers to the increase in the economy’s production over a period of time. Since economic production is measured by GDP, economic growth can simply be understood as the increase in GDP value over time.

21. What are the major sources that push forward economic growth?

Answer: The major sources that push forward economic growth are:

(i) Growth of labour force: It not only implies a quantitative increase in the labour force but also a qualitative increase which will lead to a better utilisation of resources and an increased productivity.

(ii) Capital formation: It simply implies an increase in the investment level that the economy undertakes which definitely will lead to an increased production and income.

(iii) Technological progress: It implies the development and fuller utilisation of new technology which leads to less wastage and more productivity.

22. What is inflation?

Answer: Inflation refers to a situation of constantly rising prices of commodities and factors of production in the economy.

23. What is unemployment?

Answer: Unemployment majorly refers to involuntary unemployment, where the labour is able as well as willing to work but is sitting idle due to the unavailability of any work opportunity.

24. What is a business cycle?

Answer: The business cycle, also known as the economic cycle or trade cycle, is the downward or upward movement of gross domestic product around its long-term growth trend. In other words, it describes the rise and fall in the production of goods and services in an economy.

25. What are the four phases of a business cycle?

Answer: The four phases of a business cycle are:

(i) Expansion (Boom or prosperity)

(ii) Peak (upper turning point)

(iii) Contraction (Downsizing, Recession)

(iv) Trough (or Depression) (lower turning point)

26. What is aggregate demand?

Answer: In macroeconomics, Aggregate Demand is the demand for final goods and services in an economy at a given time. It specifies the amounts of goods and services that will be purchased at all possible price levels. This is the demand for the gross domestic product of an economy.

27. What is aggregate supply?

Answer: Aggregate supply is the total supply of goods or services that firms in a national economy plan on selling during a specific time period. It is the total amount of goods and services that firms are willing and able to sell at a given price level in an economy.

28. What are consumption goods?

Answer: Goods which are consumed for their own sake or which satisfy the current wants of consumers directly are called consumption (or consumer) goods.

29. What are capital goods?

Answer: Capital goods are fixed assets of producers which are repeatedly used in the process of production for several years. Such goods are used for generating income by production units.

30. What are durable consumer goods?

Answer: Durable goods are consumer goods that can be used for consumption again and again over a considerable period of time, e.g., chairs, cars, fridges, shoes, TV-sets.

31. What are non-durable consumer goods?

Answer: Non-durable goods are like single-use goods which are used up by consumers in a single act of consumption, e.g., milk, fruits and vegetables, matches, cigarettes, coal, etc.

32. What are final goods?

Answer: All goods which are meant either (a) for consumption by consumers or (b) for investment by firms are called final goods. They are meant for final use, and the final users of a product are consumers and producers.

33. What are intermediate goods?

Answer: All goods which are used (a) as raw material for further production of other goods or (b) for resale in the same year are known as intermediate goods.

34. What is the basis of distinction between final and intermediate goods?

Answer: The basis of distinction between final and intermediate goods is the end use made of the good, not the good itself.

35. What is intermediate consumption?

Answer: Goods which are used up as raw material in the production of other goods are called intermediate consumption.

36. What is a flow variable?

Answer: A flow is a quantity which is measured with reference to a period of time. Thus, flows are defined with reference to a specific period, e.g., hours, days, weeks, months or years. It has a time dimension.

37. What is a stock variable?

Answer: A stock is a quantity which is measurable at a particular point of time, e.g., 4 p.m., 1st January, Monday, 2016, etc. A stock has no time dimension.

38. Give two examples of flow variables.

Answer: Two examples of flow variables are National Income and investment.

39. Give two examples of stock variables.

Answer: Two examples of stock variables are Population and capital.

40. What is investment?

Answer: Investment means an addition made to the stock of capital goods (such as buildings, equipment, inventory of goods) during a given period that adds to the future productive capacity of the economy. It implies the creation or addition of physical assets which are used for increasing the productive capacity of the economy in the future.

41. What is gross investment?

Answer: Gross investment is the total addition of capital goods to the existing capital stock of an economy during a time period. It is the sum of (i) expenditure on the purchase of fixed assets and (ii) expenditure on the purchase of inventory stock during a year.

42. What is depreciation?

Answer: Depreciation means the loss of value of a fixed asset (like a building or machinery) due to its normal wear and tear in the process of production.

43. What is another name for depreciation?

Answer: Another name for depreciation is consumption of fixed capital.

44. What is net investment?

Answer: Net investment is a measure of the net addition to the economy’s capital stock after deducting the depreciation of existing stock during the year.

45. How is net investment calculated?

Answer: Net investment is calculated using the formula: Net investment = Gross investment – Depreciation.

46. What is net capital formation?

Answer: Net investment is also called net capital formation. It is the net addition to the capital stock in the economy.

47. Name the four sectors of an economy.

Answer: The four sectors of an economy are the Household Sector, Producer Sector, Government Sector, and Rest of the World.

48. What does the household sector consist of?

Answer: The household sector consists of consumer goods and services, and households are also owners of the factors of production.

49. What does the producer sector consist of?

Answer: The producer sector consists of firms, i.e. all producing units in the economy. Firms hire factors of production like Land, Labour, Capital and Entrepreneurial skills from households for the production of goods and services.

50. What is the role of the government sector?

Answer: The government sector performs various welfare functions such as maintaining law and order and defence.

51. What does the ‘Rest of the World’ sector include?

Answer: The ‘Rest of the World’ sector, also called the external sector, includes all such activities which are related to the export and import of goods and capital between the domestic economy and the rest of the world.

52. Briefly distinguish between microeconomics and macroeconomics.

Answer: Microeconomics is the study of the behaviour of individual economic units of the economy, whereas macroeconomics is the study of the behaviour of the economy as a whole and its aggregates.

The main differences between the two are:

53. Explain the core beliefs of the Classical School of economic thought.

Answer: According to the Classical School of economic thought:

(i) An economy as a whole always functions at a level of full employment due to the free play of market forces in a free economy.

(ii) Supply creates its own demand.

54. How did the Great Depression challenge the classical doctrine of full employment?

Answer: Until the early 1930s, the classical doctrine of automatic full employment was largely accepted. The Great Depression of the early 1930s (1929–33) defied the idea that the automatic working of the market mechanism would ensure an equilibrium level of income consistent with the full employment of resources. Although the USA and other Western countries were highly industrialised with well-developed basic industries, electric power, means of transport and communication, banks, and other financial institutions, there was a persistent fall in the level of output, income, and employment. The Classicals could not explain this phenomenon during the worldwide depression.

55. What led to the development of modern macroeconomics?

Answer: The failure of the Classical School to explain the Great Depression led to the development of modern macroeconomics. The British economist J.M. Keynes criticised the Classical assumption of full employment and developed a new theory known as Macroeconomic Theory. During the Great Depression of 1929-33, a strong desire to control business cycles in advanced economies and to develop backward economies became the main factors that contributed to the development of modern macroeconomics.

56. Why is macroeconomics also known as the ‘Theory of Income and Employment’?

Answer: The subject matter of macroeconomics revolves around the determination of the level of income and employment; therefore, it is also known as the ‘Theory of Income and Employment’.

57. Explain any three points highlighting the importance of macroeconomics.

Answer: Three points highlighting the importance of macroeconomics are:

(i) It helps to understand the functioning of a complicated modern economic system. It describes how the economy as a whole functions and how the level of national income and employment is determined on the basis of aggregate demand and aggregate supply.

(ii) It helps to achieve the goal of economic growth, a higher level of GDP, and a higher level of employment. It analyses the forces that determine the economic growth of a country and explains how to reach the highest state of economic growth and sustain it.

(iii) It helps to bring stability to the price level and analyses fluctuations in business activities. It suggests policy measures to control inflation and deflation.

58. How does macroeconomics help in formulating correct economic policies?

Answer: With a detailed knowledge of the functioning of an economy at the macro level, it has been possible to formulate correct economic policies and also coordinate international economic policies. Correct economic policies formulated at the macro level have made it possible to control business cycles, such as inflation and deflation. As a result, violent booms and depressions have become things of the past.

59. Briefly explain the scope of macroeconomics.

Answer: Macroeconomics enriches our knowledge of the functioning of an economy by studying the behaviour of national income, output, investment, savings, and consumption. It helps in solving the problems of inflation, unemployment, economic instability, and economic growth. The scope of macroeconomics includes:

Theory of National Income: The study of macroeconomics is very important for evaluating and analysing the performance of the economy in terms of National Income. This helps in forecasting the level of economic activity and the performance of an economy globally.

Theory of Employment: The general level of employment in an economy depends upon effective demand, which in turn depends on aggregate demand and aggregate supply. Macroeconomics has special significance in studying the causes and effects of general unemployment.

Theory of Money: Macroeconomics has scope in solving monetary problems. Frequent changes in the value of money, such as inflation or deflation, affect economic activities. By analysing these changes, they can be corrected by adopting proper monetary, fiscal, and other measures for the economy as a whole.

Theory of Economic Growth: The economics of growth is also a study in macroeconomics. It is on the basis of macroeconomics that the resources and capabilities of an economy are evaluated.

60. How is the Theory of Employment a part of macroeconomics?

Answer: The general level of employment in an economy depends upon the effective demand, which in turn depends on aggregate demand and aggregate supply functions. Unemployment in an economy is caused by a deficiency of effective demand, which can be eliminated by raising total investment, total output, total income, and total consumption. Thus, macroeconomics has special significance in studying the causes and effects of general unemployment, making the Theory of Employment a part of its scope.

61. How is the Theory of Money a part of macroeconomics?

Answer: Macroeconomics has scope in solving monetary problems. Frequent changes in the value of money, such as inflation or deflation, affect economic activities. By analysing these changes, they can be corrected by adopting proper monetary, fiscal, and other measures for the economy as a whole. This makes the Theory of Money a part of macroeconomics.

62. Explain the basic macroeconomic problems of economic growth and inflation.

Answer: The basic macroeconomic problems include economic growth and inflation.

Economic Growth: This refers to the increase in an economy’s production over a period of time. Since economic production is measured by GDP, economic growth can be understood as the increase in GDP value over time. Every economy aims to continually increase its GDP and GDP growth rate to fulfil the never-ending demands of its population.

Inflation: This refers to a situation of constantly rising prices of commodities and factors of production in the economy. As a result, the purchasing power of consumers falls, leading to social implications. It harms most people but also benefits some parts of society. Beyond a certain extent, it is harmful to the entire economy because the cost of production also rises, leading to a downfall in productivity, GDP, and economic growth.

63. How does involuntary unemployment affect an economy?

Answer: Involuntary unemployment refers to a situation where labour is able as well as willing to work but is sitting idle due to the unavailability of any work opportunity. As a result of the non-utilisation of an available resource, the actual output of the economy is less than the potential output, leading the production to be at a point lower than the Production Possibility Curve (PPC). Further, the earning population decreases, leading to a greater dependency of the non-working population on such people, causing an increased income disparity.

64. Explain the difference between consumption goods and capital goods with examples.

Answer: Consumption goods are goods that are consumed for their own sake or that satisfy the current wants of consumers directly. For example, food, shirts, shoes, cigarettes, pens, TV sets, and the services of a doctor are all consumer goods because when used, they satisfy the immediate needs of consumers.

Capital goods are fixed assets of producers that are repeatedly used in the process of production for several years. Such goods are used for generating income by production units. Examples of capital goods include tools, implements, machinery, plants, tractors, buildings, and transformers.

65. How are producer goods different from capital goods?

Answer: Broadly, all goods that are used in the production of other goods are termed producer goods. They are used in two ways: as raw material, which are single-use producer goods that get merged in the final goods like wood in making furniture, and as fixed assets, which are capital goods. Capital goods are producer goods of durable use that are repeatedly used for a long time, like a plant or machinery. Capital goods include only fixed assets of producers, which are usually of high value. Thus, all capital goods are producer goods, but all producer goods are not capital goods.

66. Explain the distinction between final goods and intermediate goods using an example.

Answer: Final goods are all goods that are meant either for consumption by consumers or for investment by firms. They are meant for final use, and the final users are consumers and producers.

Intermediate goods are all goods that are used as raw material for the further production of other goods or for resale in the same year.

The basis of distinction between final and intermediate goods is the end use made of the good, not the good itself. For example, in the manufacturing of biscuits, the biscuits are final goods, but the flour, milk, sugar, and salt used in making them are intermediate goods. Similarly, cloth purchased by a household for daily use is a final good, but cloth acquired by dressmakers for making dresses is an intermediate good.

67. Why is the value of intermediate goods not included in national income?

Answer: National income includes the value of only final goods. The reason for this is that the value of intermediate goods is already included in the value of the final good when they are converted into the final good. If the value of intermediate goods is included in the estimation of national income, it will cause double counting, leading to an over-estimation of national income.

68. Distinguish between stock variables and flow variables with suitable examples.

Answer: The distinction between stock and flow variables is as follows:

69. Explain the concepts of gross investment and net investment.

Answer: Gross investment is the total addition of capital goods to the existing capital stock of an economy during a time period. It is the sum of expenditure on the purchase of fixed assets and expenditure on the purchase of inventory stock during a year. Gross investment also includes the replacement cost for the wear and tear (depreciation) that the capital stock undergoes over a period of time.

Net investment is a measure of the net addition to the economy’s capital stock after deducting the depreciation of the existing stock during the year. It is calculated by deducting depreciation from gross investment. Symbolically:

Net investment = Gross investment – Depreciation

70. What is depreciation? Why is it deducted from gross investment?

Answer: Depreciation, also known as consumption of fixed capital, is the loss of value of a fixed asset, like a building or machinery, due to its normal wear and tear in the process of production. Fixed capital such as machines, tools, and buildings wear out over a period of time when repeatedly used, leading to a fall in their value.

Depreciation is deducted from gross investment to find the net investment. Net investment is the measure of the net addition to the economy’s capital stock. Since gross investment includes the amount spent on replacing worn-out capital, this amount must be deducted to determine the actual new addition to the capital stock during a period.

71. Briefly describe the four sectors of an economy.

Answer: An economy is a place where the exchange of goods and services takes place in its four sectors. These sectors are:

(i) Household Sector: It consists of consumer goods and services, and households are also the owners of the factors of production.

(ii) Producer Sector: It consists of firms, which are all the producing units in the economy. Firms hire factors of production like land, labour, and capital from households for the production of goods and services.

(iii) Government Sector: The government performs various welfare functions, such as maintaining law and order and defence.

(iv) Rest of the World: It is also called the external sector. It includes all such activities that are related to the export and import of goods and capital between the domestic economy and the rest of the world.

72. Explain the background against which J.M. Keynes propounded his macroeconomic theory.

Answer: Till the early 1930s, the classical doctrine of automatic full employment was largely accepted. But the Great Depression of the early 1930s (1929–33) defied the myth that the automatic working of the market mechanism would ensure an equilibrium level of income consistent with the full employment of resources. Although the USA and other Western countries were highly industrialised with well-developed basic industries, electric power, means of transport and communication, banks and other financial institutions, there was a persistent fall in the level of output, income and employment. The Classicals could not explain this phenomenon during the world-wide depression.

It was against this background that the well-known British economist J.M. Keynes propounded his own theory and wrote his famous book “General Theory of Employment, Interest and Money”, published in 1936, which brought about a revolution in economic thought called the Keynesian Revolution. Keynes criticised the Classical assumption of full employment and developed a new theory known as Macroeconomic Theory.

73. “Macroeconomics is the basis of all plans of economic development.” Discuss the importance of macroeconomics.

Answer: In a suitably modified form, macroeconomics is the basis of all plans of economic development of under-developed economies. The importance of macroeconomics is as follows:

74. Explain the different theories that constitute the scope of macroeconomics.

Answer: The scope of macroeconomics includes the following theories that help to resolve the major issues or problems of an economy:

(i) Theory of National Income: The study of macroeconomics is very important for evaluating and analysing the performance of the economy in terms of National Income. With the advent of the Great Depression of the 1930’s, it became necessary to analyse the courses of general over production and general unemployment. This led to the construction of the data on national income which helped in forecasting the level of economic activity and performance of an economy globally.

(ii) Theory of Employment: The general level of employment in an economy depends upon the effective demand which in turn depends on aggregate demand and aggregate supply functions. Unemployment in an economy is caused by deficiency of effective demand which can be eliminated by raising total investment, total output, total income and total consumption. Thus, macroeconomics has special significance in studying the causes and effects of general unemployment.

(iii) Theory of Money: Macroeconomics has scope in solving monetary problems. Frequent changes in the value of money, inflation or deflation, affect the economic activities. On analysing these changes, they can be corrected by adopting proper monetary, fiscal and other measures for the economy as a whole.

(iv) Theory of Economic Growth: The economics of growth is also a study in macroeconomics. It is on the basis of macroeconomics that the resources and capabilities of an economy are evaluated. Proper planning is done to increase the level of national income, output and employment so as to raise the level of economic growth and development of an economy as a whole.

75. Differentiate between microeconomics and macroeconomics on any five grounds.

Answer: The main differences between microeconomics and macroeconomics are as under:

76. What are the basic problems of an economy at the macroeconomic level? Explain them in detail.

Answer: The basic problems posed at the macroeconomic level are Economic Growth, Inflation and Unemployment. These are explained below:

Economic growth refers to the increase in the economy’s production over a period of time. Since economic production is measured by GDP, economic growth can simply be understood as the increase in GDP value over time. Every economy strives to fulfil the never-ending demands of its population effectively and hence, they aim to continually increase their GDP and GDP growth rate. The major sources to push forward the growth are:

Thus, the ultimate issue is not only to promote economic growth but also to ensure the maintenance of the current growth level.

Inflation refers to a situation of constantly rising prices of commodities and factors of production in the economy. As a result, the purchasing power of the consumers, i.e., the real income, falls, leading to a lot of social implications. Due to continuous inflation, the cost of production also rises, thus leading to a downfall in productivity, GDP and hence, economic growth. Thus, it is necessary to maintain the inflation level to a minimal level which can be effectively done only through a proper government intervention.

Unemployment majorly refers to involuntary unemployment, where the labour is able as well as willing to work but is sitting idle due to unavailability of any work opportunity. As a result of non-utilisation of an available resource, the actual output of the economy is less than the potential output, thus leading the production to be at a point lower than the PPC. Further, the earning population decreases leading to a greater dependency of non-working population on such people causing an increased income disparity. Thus, it is a major problem faced by all the economies which needs to be addressed through government intervention and an effective fiscal policy on an immediate basis.

77. What is a business cycle? Describe its four phases with the help of a diagram.

Answer: The business cycle, also known as the economic cycle or trade cycle, is the downward or upward movement of gross domestic product around its long-term growth trend. In other words, it describes the rise and fall in the production of goods and services in an economy. The period of high income, output and employment has been called the period of expansion or prosperity and the period of low income, output, and employment has been described as the period of contraction or depression. These alternating periods of expansion and contraction in economic activity have caused the business cycle.

There are four phases of a business cycle: (i) Expansion (Boom or prosperity), (ii) Peak (upper turning point), (iii) Contraction (Downsizing, Recession), and (iv) Trough (or Depression) (lower turning point). We start from the trough or depression when the economic activity is at its lowest level. With the revival of activity, the economy moves into the expansion phase, but due to some causes, the expansion cannot continue indefinitely. After reaching a peak, contraction will start, and when the contraction gains momentum, we have a depression. The downswing continues till the lowest turning point, which is called a trough, is reached. In this way, the cycle is complete; however, after remaining at the trough for some time, the economy revives and again the new cycle begins.

78. Distinguish between final goods and intermediate goods. Provide examples to clarify the distinction.

Answer: All goods which are meant either (a) for consumption by consumers or (b) for investment by firms are called final goods. They are meant for final use and the final users of a product are consumers and producers. They are neither used for further transformation (change) in production nor resold.

All goods which are used (a) as raw material for further production of other goods or (b) for resale in the same year are known as intermediate goods. Intermediate goods are purchased by one firm from the other for use as raw material or for resale.

The basis of distinction between final and intermediate goods is the end use made of the good, not the good itself. Goods purchased and used up in the production process or resold during the same year are intermediate goods, whereas goods purchased for consumption or for investment are called final goods. For example, in manufacturing biscuits, biscuits are final goods but flour, milk, sugar, salt, etc., used in making biscuits are intermediate goods. Similarly, cloth purchased by the household for daily use is a final good but acquired by dress makers for making dresses is an intermediate good. Likewise, bread when purchased by a household is a final product but when used by the bakery for making patties is an intermediate good.

79. Explain the concepts of stock and flow. Differentiate between them with at least four points of distinction.

Answer: A stock is a quantity which is measurable at a particular point of time, e.g., 4 p.m., 1st January, Monday, 2016, etc. Capital is a stock variable. A stock has a reference to a particular date on which it shows its position and has no time dimension. Examples of stock are wealth, foreign debts, loan, inventories, opening stock, money supply, and population.

A flow is a quantity which is measured with reference to a period of time. Thus, flows are defined with reference to a specific period (length of time), e.g., hours, days, weeks, months or years. It has a time dimension. National income is a flow. Other examples of flows are expenditure, savings, depreciation, interest, exports, imports, change in inventories, and rent.

The difference between stock and flow is as follows:

80. Explain the concepts of gross investment, depreciation, and net investment. How are they related?

Answer: Gross investment is the total addition of capital goods to the existing capital stock of an economy during a time period. It is the sum of (i) expenditure on the purchase of fixed assets and (ii) expenditure on the purchase of inventory stock during a year. Gross investment also includes the replacement cost for the wear and tear (depreciation) that capital stock undergoes over a period of time.

Depreciation (consumption of fixed capital) means the loss of value of a fixed asset (like a building or machinery) due to its normal wear and tear in the process of production. Fixed capital such as machines, tools, and buildings wear out over a period of time when repeatedly used, leading to a fall in value. This fall in value due to normal wear and tear is called consumption of fixed capital.

Net investment is a measure of the net addition to the economy’s capital stock after deducting the depreciation of existing stock during the year. By deducting depreciation from gross investment, we get net investment. Net investment is also called net capital formation.

The relationship between them can be shown as:

Net investment = Gross investment – Depreciation

Gross investment = Net investment + Depreciation

81. Discuss the evolution of macroeconomic thought from the Classical School to the Keynesian Revolution. What was the role of the Great Depression in this shift?

Answer: There are two main schools of economic thought: the Classical School and the Keynesian School. According to the Classical School, an economy as a whole always functions at a level of full employment due to the free play of market forces in a free economy, and supply creates its own demand.

Till the early 1930s, the classical doctrine of automatic full employment was largely accepted. However, the Great Depression of the early 1930s (1929–33) defied the myth that the automatic working of the market mechanism would ensure an equilibrium level of income consistent with the full employment of resources. Although the USA and other Western countries were highly industrialised, there was a persistent fall in the level of output, income, and employment. The Classicals could not explain this phenomenon during the worldwide depression.

It was against this background that the well-known British economist J.M. Keynes propounded his own theory. He wrote his famous book, “General Theory of Employment, Interest and Money,” published in 1936, which brought about a revolution in economic thought called the Keynesian Revolution. Keynes criticised the Classical assumption of full employment and developed a new theory known as Macroeconomic Theory. Thus, during the Great Depression of 1929-33, a strong desire to control business cycles in advanced economies and to develop backward economies became the main factors which have contributed to the development of modern macroeconomics.

1: Who is credited with bringing about a revolution in economic thought with the publication of “General Theory of Employment, Interest and Money” in 1936?

A. Adam Smith

B. Karl Marx

C. J.M. Keynes

D. Prof. Boulding

Answer: C. J.M. Keynes

2: The study of the economy as a whole and its aggregates is known as:

A. Microeconomics

B. Macroeconomics

C. Individual Economics

D. Classical Economics

Answer: B. Macroeconomics

3: Which economic event of the early 1930s challenged the classical doctrine of automatic full employment?

A. The Industrial Revolution

B. The Great Depression

C. The Dot-com Bubble

D. The World War I economic boom

Answer: B. The Great Depression

4: According to the Classical School of economic thought, what creates its own demand?

A. Money

B. Government

C. Supply

D. Investment

Answer: C. Supply

5: Which of the following is an example of a macroeconomic aggregate?

A. A household’s income

B. A firm’s output

C. The price of a single commodity

D. National income

Answer: D. National income

6: The alternating periods of expansion and contraction in economic activity are referred to as the:

A. Fiscal Policy

B. Monetary Cycle

C. Business Cycle

D. Production Curve

Answer: C. Business Cycle

7: Goods that are used up by consumers in a single act of consumption, like milk or fruits, are classified as:

A. Capital goods

B. Durable goods

C. Intermediate goods

D. Non-durable goods

Answer: D. Non-durable goods

8: What is the term for the loss of value of a fixed asset due to normal wear and tear?

A. Investment

B. Depreciation

C. National Income

D. Inflation

Answer: B. Depreciation

9: A quantity which is measured with reference to a specific period of time, such as national income, is called a:

A. Stock variable

B. Constant variable

C. Flow variable

D. Static variable

Answer: C. Flow variable

10: Which sector of the economy consists of all producing units or firms?

A. Household Sector

B. Government Sector

C. External Sector

D. Producer Sector

Answer: D. Producer Sector

11: Goods that are meant either for consumption by consumers or for investment by firms are called:

A. Intermediate goods

B. Final goods

C. Raw materials

D. Producer goods

Answer: B. Final goods

12: The lower turning point in a business cycle, where economic activity is at its lowest level, is known as the:

A. Peak

B. Expansion

C. Trough

D. Contraction

Answer: C. Trough

13: The total demand for final goods and services in an economy at a given time is called:

A. Aggregate Supply

B. Individual Demand

C. Aggregate Demand

D. Market Equilibrium

Answer: C. Aggregate Demand

14: What is the formula for calculating Net Investment?

A. Gross Investment + Depreciation

B. Gross Investment – Depreciation

C. Gross Investment × Depreciation

D. Gross Investment / Depreciation

Answer: B. Gross Investment – Depreciation

15: The study of the behavior of individual economic units like a household or a firm falls under:

A. Macroeconomics

B. Global Economics

C. Microeconomics

D. Keynesian Economics

Answer: C. Microeconomics

16: Which of the following is NOT considered a phase of the business cycle?

A. Expansion

B. Peak

C. Stagnation

D. Trough

Answer: C. Stagnation

17: Which of the following is NOT an example of a macroeconomic aggregate?

A. Aggregate demand

B. General price level

C. Individual savings

D. National income

Answer: C. Individual savings

18: Which of the following is NOT one of the four sectors of an economy?

A. Household Sector

B. Producer Sector

C. Financial Sector

D. Rest of the World

Answer: C. Financial Sector

19: Which of the following is NOT a central problem of macroeconomics?

A. Economic Growth

B. Inflation

C. Price determination of a specific commodity

D. Unemployment

Answer: C. Price determination of a specific commodity

20: Which of the following would NOT be considered a capital good?

A. Machinery in a factory

B. A school building

C. Raw materials used in production

D. A company’s delivery truck

Answer: C. Raw materials used in production

21: Which of the following is NOT an example of a stock variable?

A. Wealth

B. Capital

C. Population

D. Investment

Answer: D. Investment

22: All of the following are considered consumption goods EXCEPT:

A. A television set purchased for a home

B. A tractor purchased by a farmer

C. A shirt purchased by a student

D. A meal at a restaurant

Answer: B. A tractor purchased by a farmer

23: The scope of macroeconomics includes all of the following theories EXCEPT:

A. Theory of National Income

B. Theory of Consumer Equilibrium

C. Theory of Employment

D. Theory of Economic Growth

Answer: B. Theory of Consumer Equilibrium

24: Assertion (A): The study of macroeconomics became prominent after the Great Depression of the 1930s.

Reason (R): The Classical School of thought could not explain the persistent fall in output, income, and employment during the worldwide depression.

A. Both A and R are true and R is the correct explanation of A.

B. Both A and R are true but R is not the correct explanation of A.

C. A is true, but R is false.

D. A is false, but R is true.

Answer: A. Both A and R are true and R is the correct explanation of A.

25: Assertion (A): The value of flour used by a bakery to make bread is not included in the calculation of national income.

Reason (R): Including the value of such intermediate goods would lead to the problem of double counting.

A. Both A and R are true and R is the correct explanation of A.

B. Both A and R are true but R is not the correct explanation of A.

C. A is true, but R is false.

D. A is false, but R is true.

Answer: A. Both A and R are true and R is the correct explanation of A.

26: Assertion (A): A country’s capital is considered a stock variable.

Reason (R): A stock variable is a quantity measured over a specific period of time.

A. Both A and R are true and R is the correct explanation of A.

B. Both A and R are true but R is not the correct explanation of A.

C. A is true, but R is false.

D. A is false, but R is true.

Answer: C. A is true, but R is false.

27: Assertion (A): A car purchased by a household is a final good.

Reason (R): Final goods are those goods which are meant only for consumption by consumers.

A. Both A and R are true and R is the correct explanation of A.

B. Both A and R are true but R is not the correct explanation of A.

C. A is true, but R is false.

D. A is false, but R is true.

Answer: C. A is true, but R is false.

28: Assertion (A): Macroeconomics is also known as the ‘Theory of Income and Employment’.

Reason (R): The primary focus of macroeconomics is the determination of the overall level of income and employment in an economy.

A. Both A and R are true and R is the correct explanation of A.

B. Both A and R are true but R is not the correct explanation of A.

C. A is true, but R is false.

D. A is false, but R is true.

Answer: A. Both A and R are true and R is the correct explanation of A.

29: Assertion (A): Gross investment is always greater than net investment, unless depreciation is zero.

Reason (R): Gross investment includes the expenditure on replacing worn-out capital, which is known as depreciation.

A. Both A and R are true and R is the correct explanation of A.

B. Both A and R are true but R is not the correct explanation of A.

C. A is true, but R is false.

D. A is false, but R is true.

Answer: A. Both A and R are true and R is the correct explanation of A.

30: Statement 1: Net investment is a stock concept.

Statement 2: Capital is a flow concept.

A. Both Statement 1 and Statement 2 are true.

B. Both Statement 1 and Statement 2 are false.

C. Statement 1 is true, but Statement 2 is false.

D. Statement 1 is false, but Statement 2 is true.

Answer: B. Both Statement 1 and Statement 2 are false.

31: (I) A refrigerator purchased by a household is a consumption good.

(II) A refrigerator purchased by a firm for its office is a capital good.

A. Statement (I) is true, but (II) is false.

B. Statement (I) is false, but (II) is true.

C. Both statements (I) and (II) are true.

D. Both statements (I) and (II) are false.

Answer: C. Both statements (I) and (II) are true.

32: (I) The study of the general price level is a subject of macroeconomics.

(II) The study of the price of tomatoes in Delhi is a subject of microeconomics.

A. Statement (I) is true, but (II) is false.

B. Statement (I) is false, but (II) is true.

C. Both statements (I) and (II) are true.

D. Both statements (I) and (II) are false.

Answer: C. Both statements (I) and (II) are true.

33: (I) Involuntary unemployment leads to the actual output of the economy being less than the potential output.

(II) Involuntary unemployment signifies a non-utilization of an available resource.

A. (I) is a contradiction of (II).

B. (I) is independent of (II).

C. (II) is the cause of (I).

D. (I) is the cause of (II).

Answer: C. (II) is the cause of (I).

34: Statement 1: All capital goods are producer goods.

Statement 2: All producer goods are capital goods.

A. Both Statement 1 and Statement 2 are true.

B. Both Statement 1 and Statement 2 are false.

C. Statement 1 is true, but Statement 2 is false.

D. Statement 1 is false, but Statement 2 is true.

Answer: C. Statement 1 is true, but Statement 2 is false.

Only for registered users