Synonyms

More meanings

Tip: select a single word for meaning & synonyms.

Select multiple words normally to copy text.

Get summaries, questions, answers, solutions, notes, extras, PDF and guide of Class 11 (first year) Economics textbook, chapter 11 Price Determination Under Perfect Competition which is part of the syllabus of students studying under AHSEC/ASSEB (Assam Board). These solutions, however, should only be treated as references and can be modified/changed.

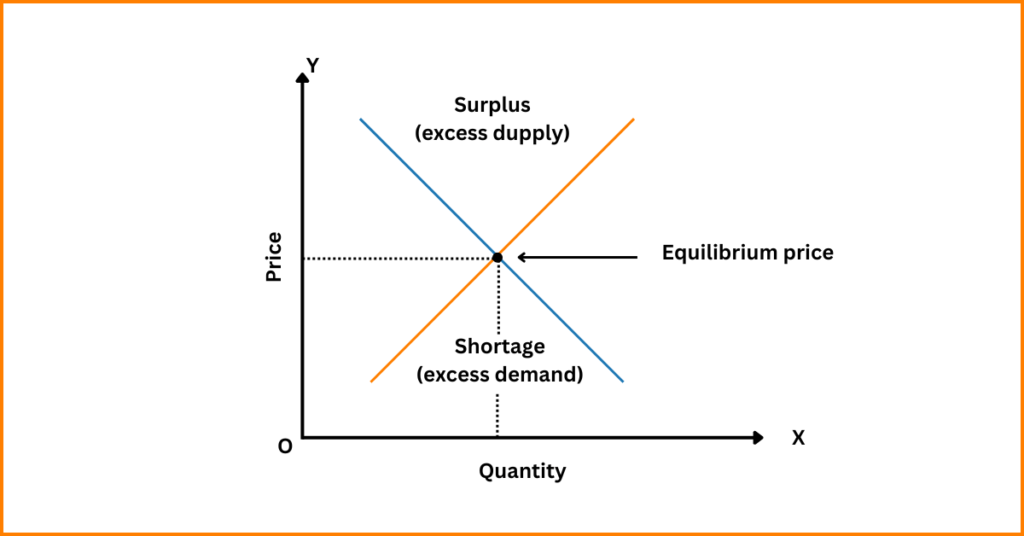

This chapter focuses on the determination of price in a perfectly competitive market. It begins by defining equilibrium price as the point where the quantity demanded by consumers equals the quantity supplied by producers. In this situation, there is no excess demand or supply. The price remains stable as long as demand and supply are balanced. Under perfect competition, no single buyer or seller can influence the market price. Instead, prices are determined by the collective actions of all buyers and sellers in the market.

The relationship between price and demand is inverse; when price decreases, demand increases. On the other hand, the relationship between price and supply is direct; producers are willing to supply more at higher prices. This relationship is explained through a table that shows how prices change depending on the balance between demand and supply.

Equilibrium price is reached when the quantity demanded equals the quantity supplied. If demand exceeds supply at a certain price, buyers will be willing to pay more, causing the price to rise until equilibrium is restored. Conversely, if supply exceeds demand, sellers will lower prices until demand increases, leading to the equilibrium price.

The concept of the “invisible hand” is introduced, a metaphor given by Adam Smith. It explains how market forces naturally adjust prices without government intervention. When there is excess demand, prices rise, and when there is excess supply, prices fall, bringing the market back to equilibrium.

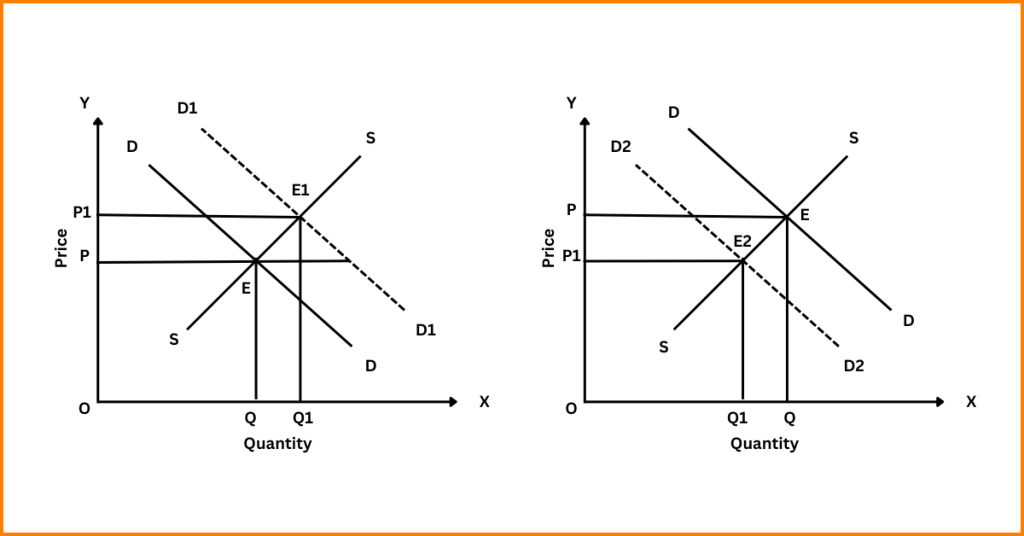

Changes in demand or supply affect the equilibrium price and quantity. An increase in demand with a constant supply will raise both price and quantity. If demand decreases, the price falls. Similarly, an increase in supply with constant demand reduces the price but increases the quantity sold. A decrease in supply raises the price while reducing the quantity sold.

The chapter also addresses situations where both demand and supply change simultaneously. For example, if both increase equally, the equilibrium price remains unchanged, but the quantity increases. However, if one changes more than the other, the effects on price and quantity differ. Finally, the determination of wages under perfect competition is briefly discussed, following similar principles of demand and supply applied to labour markets.

1. What is market equilibrium?

Answer: Market equilibrium refers to a situation where the quantity of a product demanded by consumers equals the quantity supplied by producers, resulting in no tendency for price to change.

2. Give the meaning of equilibrium price.

Answer: Equilibrium price is the price at which the quantity of a product that consumers want to buy is exactly equal to the quantity that producers want to sell.

3. What is meant by equilibrium quantity?

Answer: Equilibrium quantity refers to the quantity bought and sold at the equilibrium price.

4. How does a cost-saving technology affect the price and quantity determined?

Answer: A cost-saving technology will increase supply, which reduces the price of the product and increases the quantity produced and sold in the market.

5. What happens to the equilibrium price of a commodity when its demand rises?

Answer: When demand rises, the equilibrium price of the commodity increases, and the equilibrium quantity also increases.

6. What will be the effect of a leftward shift of the supply curve on the equilibrium price and equilibrium quantity?

Answer: A leftward shift of the supply curve will result in a higher equilibrium price and a lower equilibrium quantity.

7. How will the increase in income of the buyers of an inferior good affect the equilibrium price of the good?

Answer: An increase in income of the buyers of an inferior good will decrease the demand for the good, leading to a fall in the equilibrium price and a reduction in the equilibrium quantity.

8. What happens to the equilibrium price of a commodity, if there is a decrease in its demand and an increase in its supply?

Answer: If there is a decrease in demand and an increase in supply, the equilibrium price of the commodity will fall, and the equilibrium quantity may either increase, decrease, or remain the same depending on the magnitude of the shifts.

1. Explain market equilibrium.

Answer: Market equilibrium refers to the market situation at which the plans of consumers and producers are matched. It may be defined as a situation in which the total quantity of the commodity that all the producers are willing to sell is exactly equal to the total quantity which all the consumers of the market are prepared to buy. This implies that the total market supply will be equal to the total market demand at equilibrium.

2. With the help of a suitable diagram explain the process of determination of equilibrium price of a commodity under a perfectly competitive market.

Answer: Under perfect competition, no individual consumer or producer can influence the price of a commodity. The price of the commodity is determined by the free interaction of market forces of demand and supply.

The intersection of the demand and supply curves determines the equilibrium price and quantity. At this point, the quantity demanded equals the quantity supplied. If the price is above the equilibrium level, there will be excess supply, causing the price to fall. If the price is below the equilibrium level, there will be excess demand, causing the price to rise.

3. Explain the effect of increase in demand on equilibrium price and quantity.

Answer:

4. Explain the effects of increase in supply of a good on its equilibrium price and equilibrium quantity. Use diagram.

Answer:

Here is the diagram illustrating this effect:

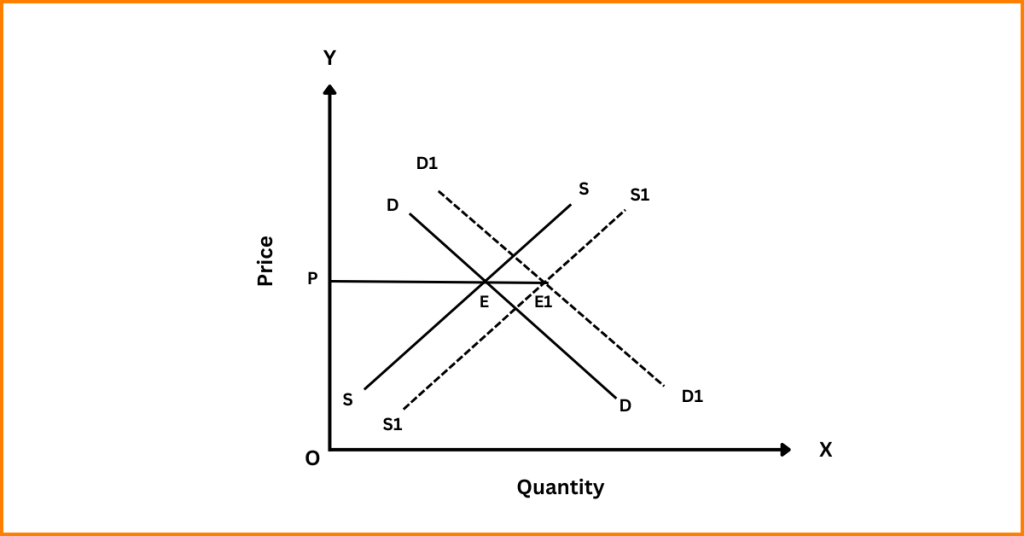

5. If at a given price of a commodity there is excess demand, how will the equilibrium price be reached? Explain with the help of a diagram.

Answer: When the quantity demanded exceeds the quantity supplied at the given price, there is excess demand. This excess demand creates competition among buyers, leading to a rise in the price of the commodity. As the price rises, the quantity demanded decreases (contraction of demand), and the quantity supplied increases (expansion of supply). This process continues until the quantity demanded equals the quantity supplied, and a new equilibrium price is established.

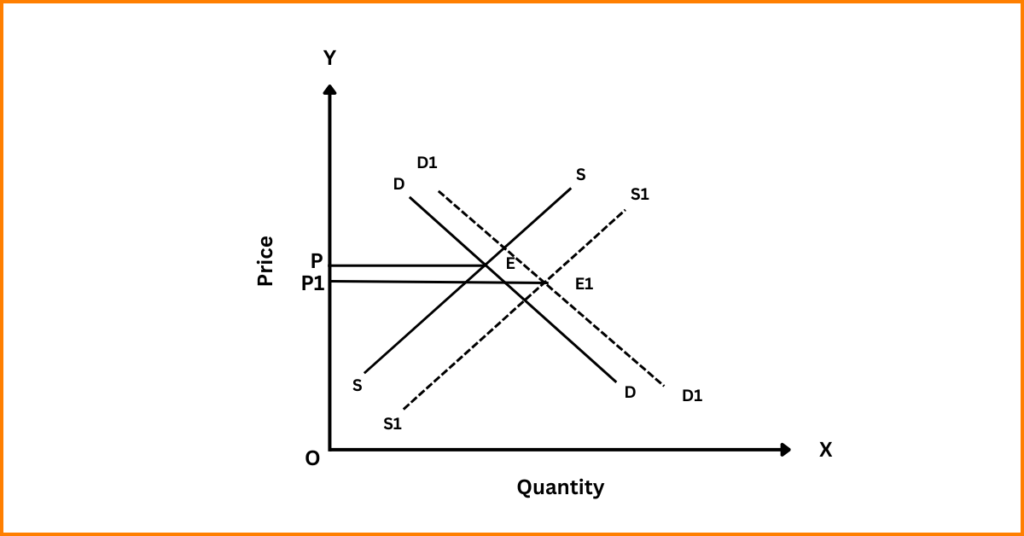

6. Explain the chain of effects of excess supply on equilibrium price.

Answer: Chain of effects of excess supply:

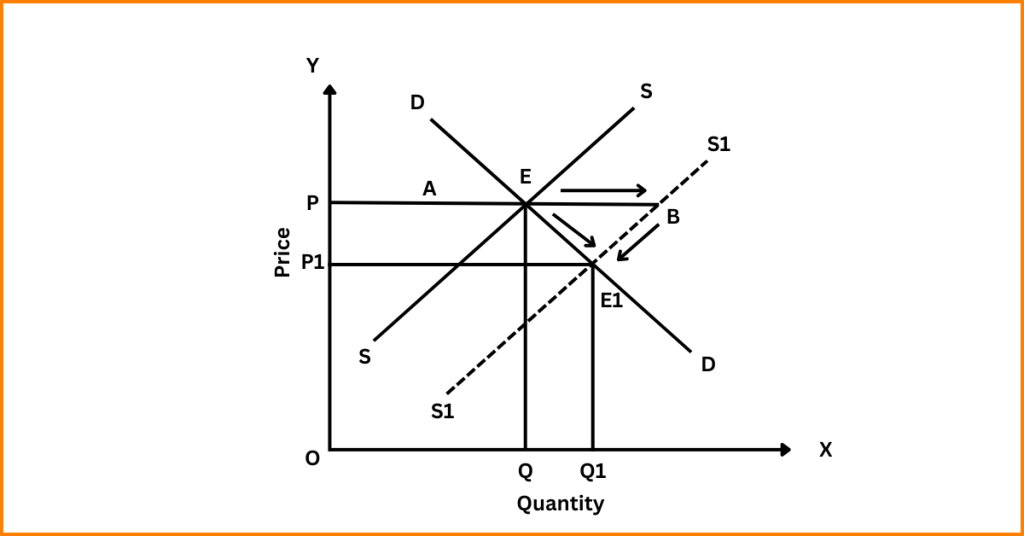

Answer: When the supply curve shifts rightward, it indicates an increase in supply while demand remains unchanged. This creates excess supply at the existing equilibrium price. To sell the surplus, producers reduce the price, leading to a contraction in supply and an expansion in demand. The process continues until a new equilibrium is reached at a lower price and higher quantity.

7. How are equilibrium price and quantity affected when income of the consumers (a) increase (b) decrease?

Answer: (a) An increase in income of buyers will increase the demand at the given price. It will lead to a situation of excess demand in the market which leads to competition among buyers. This will raise the market price. Increase in price leads to rise in supply (i.e., expansion in supply) and fall in demand (i.e., contraction in demand). These changes would continue till supply and demand become equal at a new equilibrium price. As there is an increase in demand only, equilibrium price will rise.

(b) A decrease in income leads to reduce the demand at the given price. It will lead to excess supply in the market. This leads to competition among sellers, which reduces the price. Fall in price leads to reduction in supply (i.e., contraction in supply) and rise in demand (expansion of demand). These changes would continue till supply and demand become equal at a new equilibrium price. As there is a fall in demand only, both equilibrium price and equilibrium quantity will fall.

8. How do the equilibrium price and quantity of a commodity change when the price of input used in its production changes?

Answer: A rise in the price of inputs will increase the cost of production, causing a leftward shift in the supply curve. This leads to a higher equilibrium price and a lower equilibrium quantity. Conversely, if the price of inputs falls, the cost of production decreases, causing a rightward shift in the supply curve. This results in a lower equilibrium price and a higher equilibrium quantity.

9. If the price of a substitute (Y) of good X falls, what impact does it have on the equilibrium price and quantity of good X?

Answer: If the price of a substitute (Y) of good X falls, the demand for good X will decrease as consumers will shift their consumption to the cheaper substitute Y. This leads to a leftward shift of the demand curve for good X, causing both the equilibrium price and equilibrium quantity of good X to fall.

10. A severe drought results in a drastic fall in the output of wheat. Analyze how it will affect the market price of wheat.

Answer: A severe drought that causes a drastic fall in the output of wheat will shift the supply curve leftward, creating excess demand in the market. This will lead to competition among buyers, pushing the market price of wheat upwards. Thus, the equilibrium price will increase, while the equilibrium quantity will decrease.

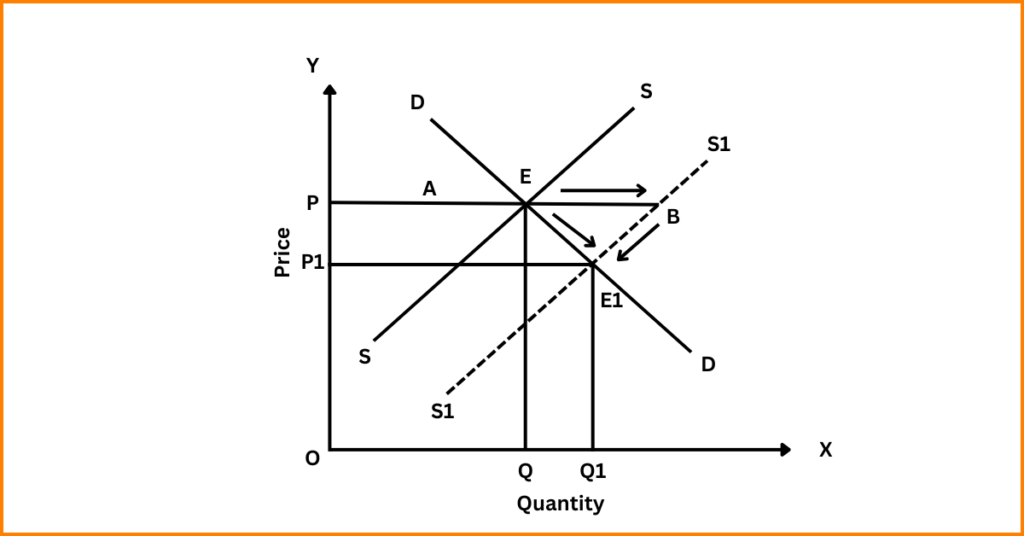

11. Explain with help of a diagram the effect of a rightward shift of supply curve of a commodity on its equilibrium price and quantity.

Answer: When the supply curve shifts rightward, it indicates an increase in supply at every price level. As a result, the equilibrium price falls, and the equilibrium quantity increases. In the diagram, the original equilibrium point is shown where the original supply curve intersects the demand curve. The new equilibrium point, after the rightward shift of the supply curve, shows a lower price and a higher quantity.

1. ‘Under perfect competition industry is price-maker and firm the price-taker’. Explain.

Answer: Under perfect competition, an individual firm is a price-taker because the market consists of a large number of buyers and sellers, and each seller supplies a very small portion of the total market supply. Due to this, no single firm has the ability to influence the market price. The market price is determined by the collective actions of all the firms in the industry through the forces of demand and supply. The industry, as a whole, determines the price at which the commodity will be bought and sold. Once the price is established, each individual firm has to accept this price and can only adjust the quantity of output it produces. If a firm attempts to sell its product at a price higher than the market price, it will not find buyers since identical products are available at a lower price. Conversely, if the firm charges less, it will face a loss. Hence, the firm is a price-taker, and the industry is the price-maker.

2. Define perfect competition. How is price determined in a perfectly competitive market? Draw demand curve of a firm in such a market.

Answer: Perfect competition is defined as a market structure characterized by a large number of buyers and sellers, homogeneity of the product, free entry and exit of firms, and perfect knowledge of the market. In such a market, no single buyer or seller can influence the price of the product.

Price is determined by the intersection of the market demand and market supply curves. The demand curve slopes downward from left to right, indicating that with a fall in the price of the product, its quantity demanded increases, and vice versa. The supply curve slopes upward, indicating that with a rise in the price, its quantity supplied increases, and vice versa. The point where these curves intersect is called the equilibrium point. At this point, the equilibrium price and equilibrium quantity are determined. Individual firms take this price as given and produce the quantity where their marginal cost equals the price.

The demand curve of a firm in a perfectly competitive market is perfectly elastic, represented by a horizontal line at the level of the market price. This indicates that a firm can sell any quantity of the product at the market price but cannot influence the price.

3. Define equilibrium price. How is it determined? Explain with the help of a schedule.

Answer: Equilibrium price is the price at which the quantity of a product demanded by consumers is equal to the quantity supplied by producers. At this price, the market is in equilibrium, and there is neither excess supply nor excess demand.

Equilibrium price is determined through the interaction of market demand and supply. When the quantity demanded equals the quantity supplied, the price at which this equality occurs is called the equilibrium price. The determination of equilibrium price can be illustrated with the help of a demand and supply schedule:

| Price per unit (₹) | Market Demand (Units) | Market Supply (Units) | Remarks |

|---|---|---|---|

| 1 | 500 | 100 | Excess Demand |

| 2 | 400 | 200 | Excess Demand |

| 3 | 300 | 300 | Equilibrium |

| 4 | 200 | 400 | Excess Supply |

| 5 | 100 | 500 | Excess Supply |

In this schedule, the equilibrium price is ₹3, at which the quantity demanded and quantity supplied are both 300 units. Any price above ₹3 would lead to excess supply, and any price below ₹3 would lead to excess demand.

4. Explain the changes that take place when market price is greater than the equilibrium price. Use diagram.

Answer: When the market price is greater than the equilibrium price, the quantity supplied exceeds the quantity demanded, resulting in excess supply. This situation causes competition among sellers, as they are unable to sell their entire stock at the higher price. To attract buyers and sell their surplus goods, sellers start reducing the price. As the price falls, the quantity demanded increases and the quantity supplied decreases. This process continues until the price reaches the equilibrium level, where the quantity demanded equals the quantity supplied.

5. Explain the changes that take place when market price is less than the equilibrium price. Use diagram.

Answer: When the market price is less than the equilibrium price, quantity demanded will exceed quantity supplied, causing a shortage of the commodity in the market. This shortage induces competition among buyers, who are willing to pay a higher price to secure the product. As a result, the price will start rising. As the price increases, the quantity demanded will decrease (i.e., contraction in demand), and the quantity supplied will increase (i.e., expansion in supply). This process continues until the price rises to the equilibrium level, where the quantity demanded equals the quantity supplied, and the market clears. The diagram below illustrates this adjustment process.

6. Explain the concept of market equilibrium with the help of demand and supply curve. With the same diagram trace out the situations of excess demand and excess supply…

Answer: Market equilibrium refers to the situation where the quantity of a commodity demanded by consumers is equal to the quantity supplied by producers at a certain price level. This point is known as the equilibrium price and equilibrium quantity. At this price, there is no tendency for the market price to change because the plans of both consumers and producers are satisfied.

To illustrate, consider a demand and supply curve. The demand curve slopes downward from left to right, showing the inverse relationship between price and quantity demanded. The supply curve slopes upward from left to right, indicating the direct relationship between price and quantity supplied. The point where these two curves intersect represents the equilibrium point.

7. Explain how is wage determined under perfect competition.

Answer: Under perfect competition, the wage rate is determined by the interaction between the demand and supply of labor. This theory is also known as the “Demand and Supply Theory of Wages.” Wage determination under perfect competition can be explained as follows:

8. Show and explain how market equilibrium changes with the shifting of the demand curve.

Answer: Market equilibrium changes when there is a shift in the demand curve, which can happen due to factors such as changes in consumer income, preferences, or prices of related goods. The shift can be either to the right (increase in demand) or to the left (decrease in demand).

9. Show and explain how market equilibrium changes due to the shifting of supply curve.

Answer: When the supply curve shifts, market equilibrium is affected. If the supply curve shifts rightward, there is an increase in supply. As a result, there is excess supply at the original equilibrium price. This excess supply puts downward pressure on the price. As the price falls, the quantity demanded increases (expansion in demand), and the quantity supplied decreases (contraction in supply) until a new equilibrium is reached at a lower price and higher quantity.

On the other hand, if the supply curve shifts leftward, there is a decrease in supply. As a result, there is excess demand at the original equilibrium price. This excess demand puts upward pressure on the price. As the price rises, the quantity demanded decreases (contraction in demand), and the quantity supplied increases (expansion in supply) until a new equilibrium is reached at a higher price and lower quantity.

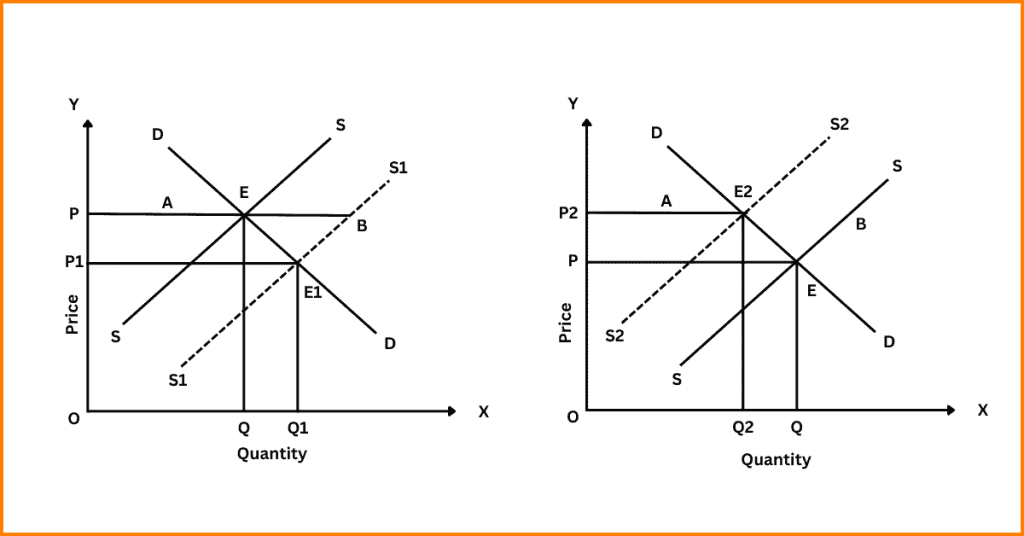

10. Explain diagrammatically the impact of simultaneous shift of demand and supply on equilibrium price and quantity.

Answer: The possible situations in this regard which are as follows:

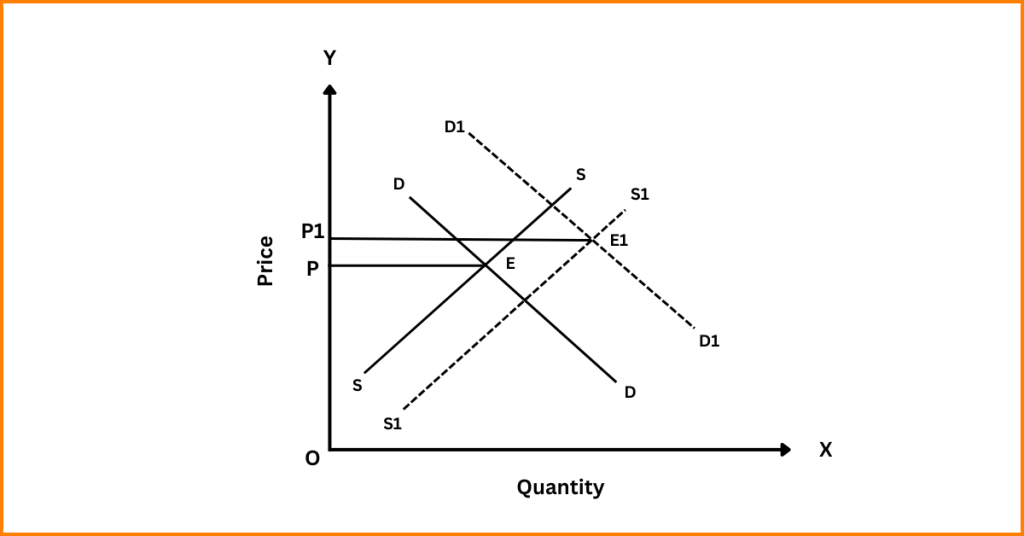

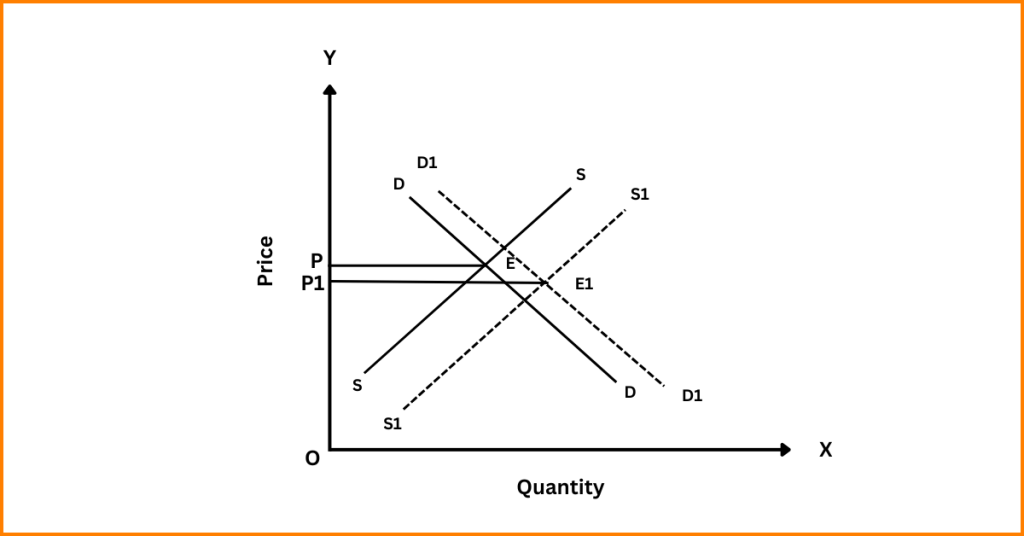

(a) When increase in demand and supply are equal: In this situation, DD and SS are the original demand and supply curves, respectively, whereas broken lines D₁D₁ and S₁S₁ represent the increase in demand and increase in supply, respectively. The changes in demand and supply are equal. Hence, the old and new equilibrium prices are the same, i.e., OP. But the new equilibrium quantity increases from PE to PE₁.

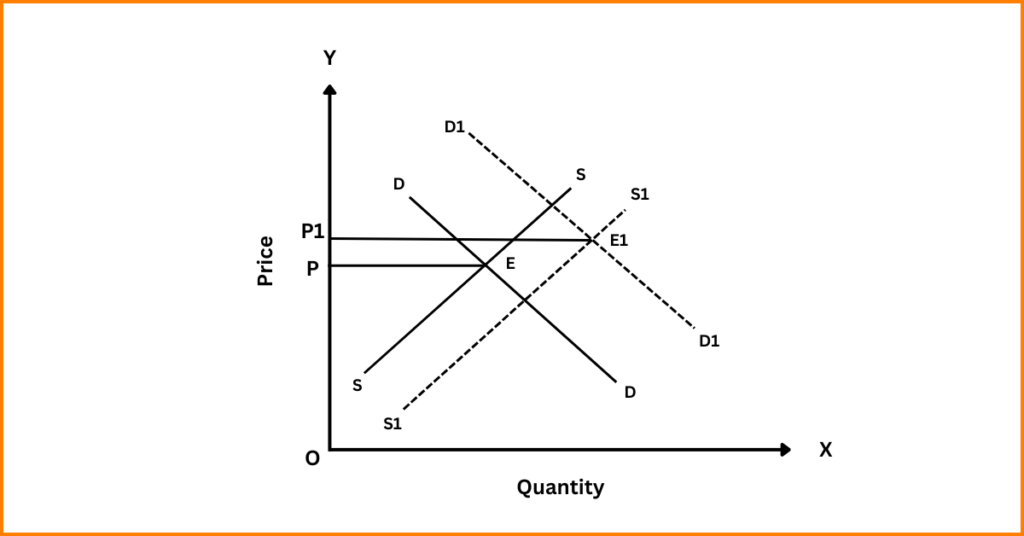

(b) When increase in supply is more than increase in demand: This depicts a situation where the increase in supply is more than the increase in demand. As a result of the shift in the demand curve from DD to D₁D₁, the supply curve shifts from SS to S₁S₁. Here, the increase in supply is more than the increase in demand. Consequently, the equilibrium price falls from OP to OP₁, but the equilibrium quantity increases from PE to PE₁.

(c) When increase in supply is less than increase in demand: This shows the effect of a simultaneous increase in demand and supply when the increase in supply is less than the increase in demand. In such a case, both the equilibrium price and quantity increase. OP is the original equilibrium price and PE is the equilibrium quantity. The demand curve D₁D₁ reflects the situation of an increase in demand, while the supply curve S₁S₁ represents the increase in supply. The increase in supply is less compared to the increase in demand. As a consequence, the new equilibrium price rises to OP₁, and the new equilibrium quantity also increases from PE to PE₁.

11. Explain graphically that with free entry and exit in a perfectly competitive market the equilibrium price is always equal to the minimum average cost of the firms.

Answer: In a perfectly competitive market, the presence of free entry and exit ensures that firms earn only normal profit in the long run. If the prevailing market price is higher than the minimum average cost (AC), existing firms earn supernormal profits. This attracts new firms into the industry, increasing the market supply and causing the price to fall. The entry of new firms continues until the price falls to the level of the minimum average cost, where firms earn only normal profit.

Conversely, if the market price is lower than the minimum average cost, existing firms incur losses. Some firms will exit the market, decreasing the market supply and causing the price to rise. This exit process continues until the price increases to the level of the minimum average cost, eliminating losses. As a result, in the long run, the equilibrium price in a perfectly competitive market is always equal to the minimum average cost of the firms.

12. Does the shift in the demand curve have any impact on the equilibrium price if the condition of free entry and exit prevails? Explain.

Answer: Under the condition of free entry and exit in a perfectly competitive market, a shift in the demand curve does not have a lasting impact on the equilibrium price. When there is an increase in demand, the demand curve shifts to the right, causing a temporary increase in the equilibrium price. The rise in price attracts new firms to enter the market, which increases the supply. The increased supply eventually brings the price back to the original level. Similarly, if there is a decrease in demand and the demand curve shifts to the left, the equilibrium price temporarily falls. However, some firms will exit the market due to reduced profitability, which decreases the supply and raises the price back to its original level. Thus, in the long run, the equilibrium price remains unchanged, but the equilibrium quantity will adjust according to the change in demand.

13. Explain the effect of price-ceiling on market equilibrium under the condition of perfect competition.

Answer: Price ceiling refers to the situation when the government sets a maximum price for a commodity, which is lower than the equilibrium price. This is generally done to ensure that essential commodities remain affordable for the general public. Under perfect competition, when a price ceiling is imposed, the quantity demanded of the commodity increases because of the lower price, but the quantity supplied decreases as producers are less willing to supply at this lower price. This results in excess demand or a shortage in the market.

The shortage created by the price ceiling means not all consumers will be able to purchase the commodity at the lower price. Some consumers may resort to non-price competition, like standing in long queues or forming connections to secure the product. Additionally, the quality of the product may deteriorate as producers have no incentive to maintain high standards when they cannot charge higher prices. In some cases, a black market may emerge where the commodity is sold at a higher price than the ceiling price.

1. The demand and supply curve of a firm under perfectly competitive market are given below: D = 500 – P, S = 250 + 4P, Where P = Price level, D = Quantity demanded, S = Quantity supplied. Find out the equilibrium level of price (P). (AHSEC Question Bank)

Answer: At equilibrium:

D = S

500 – P = 250 + 4P

500 – 250 = 4P + P

250 = 5P

P = 50

Equilibrium quantity:

D = 500 – P

D = 500 – 50 = 450

Equilibrium Price = 50, Equilibrium Quantity = 450

2. The demand (D) and supply curve (S) of a firm is given below, D = 100 – P, S = -25 + 4P, Where D = Quantity demanded, S = Quantity supplied, P = Price level. Find out the equilibrium level of price (P). (AHSEC Question Bank)

Answer: At equilibrium:

D = S

100 – P = -25 + 4P

100 + 25 = 4P + P

125 = 5P

P = 25

Equilibrium quantity:

D = 100 – P

D = 100 – 25 = 75

Equilibrium Price = 25, Equilibrium Quantity = 75

3. The supply and demand function of a firm in a perfectly competitive market is given below: D = 50 – 2P, S = -25 + 3P, Where, P = Price, D = Demand, S = Supply. (AHSEC Question Bank)

Answer: At equilibrium:

D = S

50 – 2P = -25 + 3P

50 + 25 = 3P + 2P

75 = 5P

P = 15

Equilibrium quantity:

D = 50 – 2P

D = 50 – 2 × 15 = 20

Equilibrium Price = 15, Equilibrium Quantity = 20

4. The demand and supply function of a firm under perfectly competitive market are given: D = 100 – P, S = -30 + 4P, Where D = Quantity demanded, S = Quantity supplied, P = Price.

Now, (i) Find out the equilibrium level of price and output. (ii) If the government imposes a tax of ₹5 on each unit of output, find out the impact on equilibrium level of price and output. (AHSEC Question Bank)

Answer: (i) At equilibrium:

D = S

100 – P = -30 + 4P

100 + 30 = 4P + P

130 = 5P

P = 26

Equilibrium quantity:

D = 100 – P

D = 100 – 26 = 74

Equilibrium Price = 26, Equilibrium Quantity = 74

(ii) New supply function after tax: The tax of ₹5 per unit shifts the supply function to:

S = -30 + 4(P – 5)

S = -30 + 4P – 20

S = -50 + 4P

At equilibrium:

D = S

100 – P = -50 + 4P

100 + 50 = 4P + P

150 = 5P

P = 30

Equilibrium quantity:

D = 100 – P

D = 100 – 30 = 70

Equilibrium Price = 30, Equilibrium Quantity = 70

5. The demand and supply functions of a salt-producing firm under perfectly competitive market are given below: Qd = 200 – 2P and Qs = -100 + 3P.

Now, (i) Find out the equilibrium level of output and price. (ii) If due to increased cost the supply function becomes Qs = -200 + 3P, what will be the change in equilibrium price and quantity? Do you think that these changes are expected? (AHSEC Question Bank)

Answer: (i) At equilibrium:

Qd = Qs

200 – 2P = -100 + 3P

200 + 100 = 3P + 2P

300 = 5P

P = 60

Equilibrium quantity:

Qd = 200 – 2P

Qd = 200 – 2 × 60 = 80

Equilibrium Price = 60, Equilibrium Quantity = 80

(ii) New supply function: Qs = -200 + 3P

At equilibrium:

Qd = Qs

200 – 2P = -200 + 3P

200 + 200 = 3P + 2P

400 = 5P

P = 80

Equilibrium quantity:

Qd = 200 – 2P

Qd = 200 – 2 × 80 = 40

Equilibrium Price = 80, Equilibrium Quantity = 40

1. Under perfect competition, what determines the price of a product?

A. A single consumer

B. A single firm

C. Government

D. Market forces of demand and supply

Answer: D. Market forces of demand and supply

Q. What happens when the demand for a product exceeds its supply at a price of ₹2?

A. Price will fall

B. Supply will increase

C. Price will rise

D. Demand will fall

Answer: C. Price will rise

Q. In the case of excess supply, what tends to happen to the price?

A. Price rises

B. Price falls

C. Price remains stable

D. Price fluctuates

Answer: B. Price falls

Q. Who introduced the concept of the ‘invisible hand’ that stabilizes the market?

A. J.S. Mill

B. David Ricardo

C. Adam Smith

D. John Keynes

Answer: C. Adam Smith

Q. What is the assumption about the supply curve in a market?

A. It slopes downward

B. It slopes upward

C. It is horizontal

D. It is vertical

Answer: B. It slopes upward

Q. If both demand and supply increase equally, what happens to the equilibrium price?

A. It falls

B. It rises

C. It remains the same

D. It fluctuates

Answer: C. It remains the same

Q. In the determination of wage rate under perfect competition, wage is equal to what?

A. Marginal Revenue Product

B. Marginal Cost

C. Value of Marginal Product

D. Total Revenue

Answer: C. Value of Marginal Product

Q. What happens when the wage rate increases beyond a certain level according to the backward-sloping supply curve?

A. Supply of labour increases

B. Supply of labour decreases

C. Demand for labour increases

D. Demand for labour decreases

Answer: B. Supply of labour decreases

Q. In the case of a decrease in both demand and supply, but the decrease is more in demand, what happens to the equilibrium price?

A. Price rises

B. Price falls

C. Price remains unchanged

D. Price fluctuates

Answer: B. Price falls

Q. What happens to the equilibrium price if there is an increase in demand but supply remains unchanged?

A. Price falls

B. Price rises

C. Price remains the same

D. Price fluctuates

Answer: B. Price rises

Q. Under perfect competition, what determines the wage rate?

A. Government regulation

B. Supply and demand of labour

C. Union negotiations

D. Individual firm decisions

Answer: B. Supply and demand of labour

Q. What is the maximum price policy also known as?

A. Price floor

B. Price ceiling

C. Price support

D. Market equilibrium

Answer: B. Price ceiling

Q. What happens when the government sets a maximum price below the equilibrium price?

A. Excess supply

B. Surplus

C. Excess demand

D. Equilibrium

Answer: C. Excess demand

Q. What is one potential consequence of price ceiling policies?

A. Increase in demand

B. Black market

C. Decrease in demand

D. Equilibrium

Answer: B. Black market

Q. When the government fixes a minimum price higher than the equilibrium price, what is this policy called?

A. Price ceiling

B. Price support

C. Price equilibrium

D. Demand control

Answer: B. Price support

Q. What happens to excess supply under a price support policy?

A. Government purchases it

B. Sellers reduce prices

C. It is sold in black markets

D. Supply is reduced

Answer: A. Government purchases it

Q. In the FAD theory by Amartya Sen, what causes food prices to rise beyond the reach of poor people?

A. High demand

B. Government policies

C. Natural calamities

D. Price control

Answer: C. Natural calamities

Q. In the FAD theory, which group faces starvation when the price of rice rises?

A. Rich families

B. Poor families

C. Middle-class families

D. All families

Answer: B. Poor families

19. What happens to the equilibrium quantity when both demand and supply decrease but the demand decrease is larger than the supply decrease?

A. It increases

B. It decreases

C. It remains unchanged

D. It fluctuates

Answer: B. It decreases

1. What is the meaning of equilibrium price?

Answer: Equilibrium price is that price at which its two determinants—demand and supply—are in balance or equal. So long as these determinants remain in the state of balance, equilibrium price would not change. At equilibrium price, quantity demanded and quantity supplied are equal. The quantity demanded and supplied at equilibrium price is called equilibrium quantity. This is also called market equilibrium. In the situation of market equilibrium, all the sellers are able to find buyers, and all the buyers are able to find sellers. There is neither excess demand nor excess supply in the market of a product.

Q. How is the equilibrium price determined under perfect competition?

Answer: Under perfect competition, no single firm or consumer can influence the price due to their negligible share in total market supply or total market demand. Price is determined by the collective actions of all firms and consumers in the market, also called the industry. Market demand is inversely related to price, meaning as the price of a good falls, the demand for that good rises. Market supply is directly related to price, meaning producers are willing to supply more only at a higher price.

At equilibrium price, quantity demanded equals quantity supplied. For example, at a price of ₹3 per unit, the quantity demanded and supplied is 300 units, which is the equilibrium quantity. If the price is higher or lower than this, either excess supply or excess demand will drive the price back to ₹3.

Q. Why is equilibrium price determined at the level where demand equals supply?

Answer: Equilibrium price is determined at the level where demand equals supply because if the price is lower or higher than this point, adjustments will occur to restore equilibrium. For example, if the price is ₹2, demand exceeds supply, leading to consumers offering a higher price, which raises the price until it reaches ₹3. Similarly, if the price is ₹4, supply exceeds demand, leading producers to lower their prices to attract more customers until the price settles back at ₹3. This process continues until market equilibrium is achieved where neither excess demand nor supply exists.

Q. What is the effect of a shift in demand on equilibrium price and quantity?

Answer: A shift in demand, which means an increase or decrease in demand due to factors other than price, impacts equilibrium price and quantity.

Q. What happens when supply shifts while demand remains unchanged?

Answer: A shift in supply, due to factors other than price, affects equilibrium price and quantity.

Q. What are the assumptions behind the concept of equilibrium price?

Answer: The concept of equilibrium price is based on the following assumptions:

Q. What is the concept of the ‘invisible hand’ in market equilibrium?

Answer: The ‘invisible hand’ concept, introduced by Adam Smith, explains how market equilibrium is achieved without external intervention. Whenever there is an imbalance in the market, the invisible hand comes into play. In the case of excess demand, it raises the price, and in the case of excess supply, it lowers the price. This process continues until the market reaches equilibrium, where demand equals supply, and prices stabilize. J.S. Mill described this by saying, “Demand, supply, and price are like three sections of a mechanism which always act and react upon one another and always tend to a state of equilibrium.”

Q. What happens when both demand and supply increase?

Answer: When both demand and supply increase, three possibilities arise:

(a) When the increase in demand and supply are equal: The equilibrium price remains unchanged, but the equilibrium quantity increases.

(b) When the increase in supply is more than the increase in demand: The equilibrium price decreases, and the equilibrium quantity increases.

(c) When the increase in supply is less than the increase in demand: Both the equilibrium price and the equilibrium quantity increase.

Q. What happens when both demand and supply decrease?

Answer: When both demand and supply decrease, there are three possible outcomes:

(a) When the decrease in demand and supply are equal: The equilibrium price remains the same, but the equilibrium quantity decreases.

(b) When the decrease in demand is more than the decrease in supply: Both the equilibrium price and the equilibrium quantity fall.

(c) When the decrease in demand is less than the decrease in supply: The equilibrium price increases, and the equilibrium quantity decreases.

Q. How is the wage rate determined under perfect competition?

Answer: The wage rate is determined by the interaction between the demand and supply of labour. Under perfect competition, firms will employ labour up to the point where the wage rate equals the value of marginal product (VMP). Firms reduce the demand for labour at higher wages and increase it at lower wages. The supply curve of labour slopes upward, meaning more workers are willing to work at higher wage rates. Wage rate equilibrium is reached when the market demand for labour equals the market supply of labour.

Q. Explain the productivity concepts related to labour.

Answer: The main concepts related to labour productivity are:

(i) Marginal Physical Product (MPP): The change in total output when the employment of a factor changes.

(ii) Value of Marginal Product (VMP): The market value of the marginal physical product (MPP), calculated as VMP = MPP × Price.

(iii) Marginal Revenue Product (MRP): The change in total revenue when the employment of a factor changes, calculated as MRP = MPP × Marginal Revenue.

(iv) Value of Average Product (VAP): The market value of the average product, calculated as VAP = Average Product × Price.

Q. What is the Maximum Price Policy (Price Ceiling Policy)?

Answer: The maximum price policy, or price ceiling policy, is when the government sets a maximum allowable price for essential goods, like rice or wheat, to ensure that poorer sections of society can afford them. If the maximum price is set below the equilibrium price, producers supply less while consumers demand more, leading to excess demand. This can result in black markets and the need for rationing.

Q. What is the Price Support Policy (Floor Price Policy)?

Answer: The price support policy, also known as the floor price policy, is when the government sets a minimum price above the equilibrium price to protect producers. For example, in agriculture, the government sets a minimum support price for crops like wheat and sugarcane. If there is excess supply, the government buys the surplus at the support price to prevent prices from falling.

14. Explain the FAD Theory of Famines by Prof. Amartya Sen.

Answer: The FAD (Food Availability Decline) theory explains that poor people suffer from food shortages due to natural calamities like droughts or floods, which reduce the production of staple foods. As a result, the price of food rises beyond the reach of the poor, leading to starvation. Prof. Amartya Sen illustrated this by showing how rising prices progressively exclude poorer families from affording staple foods like rice, causing famine conditions.

Only for registered users